Yes, you need a cash-out re-finance buying a moment home. A money-out refinance can provide you with a massive lump sum so you can be used for all you require. Residents either question if they can use money off their refi and make a down payment towards the a new possessions. If you have the monetary method for create a couple of mortgages, a money-aside refi was a great way on how best to supply a sizable down-payment.

Thankfully, you’ll be able getting homeowners to use an earnings-away re-finance to invest in second property. Whenever you are thinking about to get one minute possessions, you will understand just how cash-aside refinancing work and just how you might meet the requirements.

The whole process of obtaining a cash-away refinance to order second homes is much like the process off obtaining your brand new financial. Your own lender often request factual statements about your earnings, possessions, and you can debts to ensure to pay the loan. Likewise, you’ll want to schedule property appraisal to decide simply how much your home is worthy of. This permits the bank so you’re able to estimate simply how much you might take-out.

You need to discovered funds payment in a few days out of closing into the refinance. Once you have money, they are utilised the objective. Some home owners wait to begin with their house research until it located their cash in the re-finance, although some begin finding a moment household before it romantic with the refi.

As dollars-away refinances is actually riskier on lender, consumers can get face more strict criteria whenever obtaining cash-aside refinances to invest in next residential property. Very lenders need a credit history of at least 620 to own a beneficial refinance. Concurrently, you will probably you need a debt-to-earnings ratio away from 43% otherwise shorter, and therefore just about 43% of one’s month-to-month income can go to the home loan repayments or other bills.

The main significance of an earnings-away refi is to try to convey more than simply 20% collateral throughout the property. Loan providers always require consumers to keep at the least 20% equity whenever refinancing, but you can get any most collateral when you paydayloancolorado.net/peoria/ look at the cash. Such, for those who owe $140,000 to your a beneficial $2 hundred,000 assets, you have 30% guarantee yourself. A funds-away refi of 80% of the residence’s value wide variety in order to $160,000. Very first, the cash might possibly be used to pay-off your modern home loan harmony off $140,000. Now, you should use the rest $20,000 as the a deposit on the next domestic.

There are some positive points to using bucks-out refinances to buy second house. Even when a cash-out refi might have a slightly large interest than simply good antique refi, their interest into the a great refinance might be far lower than simply your rates for the a consumer loan or another types of financial obligation. Whenever you are looking to availableness adequate cash having a down payment, an earnings-out refi is one of the most pricing-effective selection.

Getting cash out to find second home is specially useful in specific market conditions. In the event the home values are beginning to rise quickly close by, you will possibly not must hold back until it can save you right up an excellent advance payment. Because of the doing finances-aside refi and purchasing the second domestic as quickly as possible, you could secure a lower rate into possessions up until the worthy of rises.

Other lending options

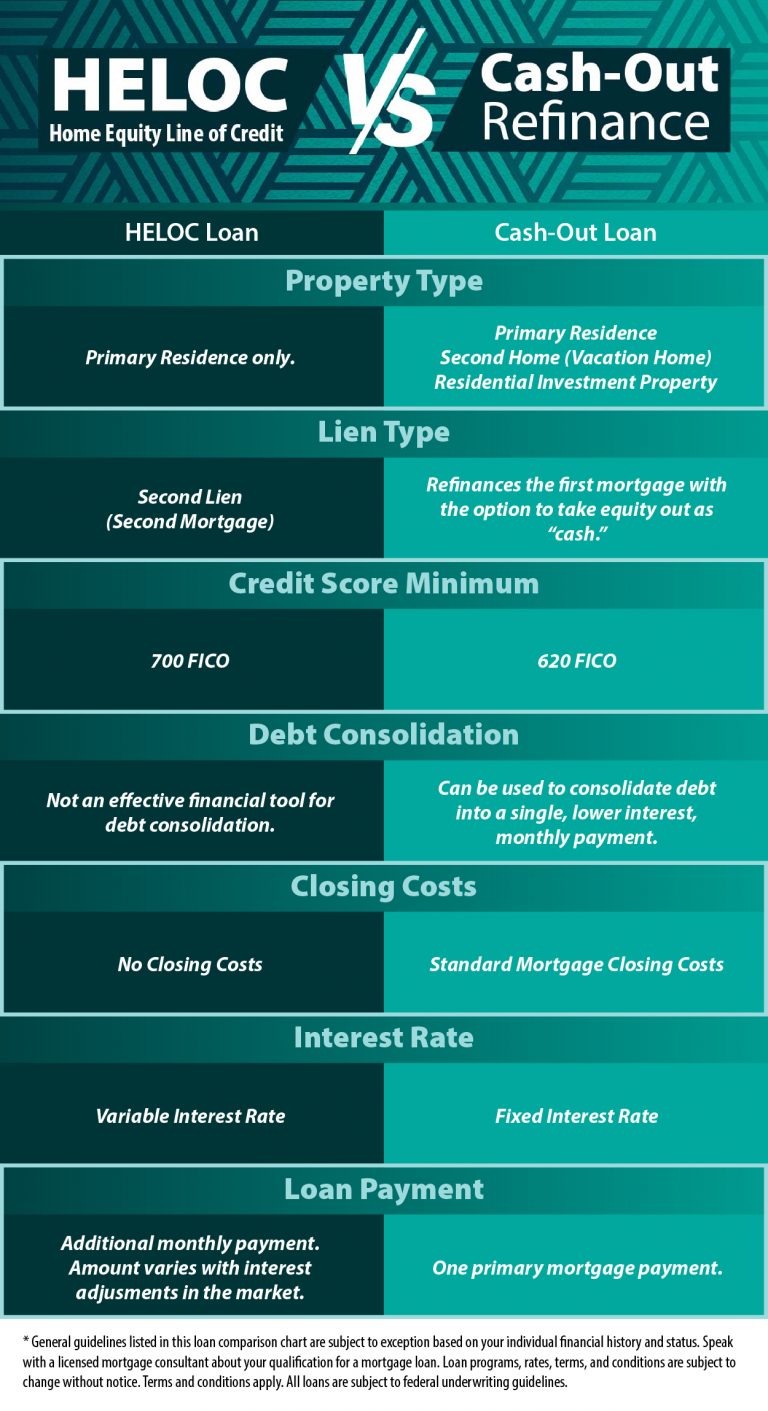

Home owners which have security in their primary homes has other options within the inclusion so you’re able to bucks-aside refinances buying next property. For example, you could potentially go for a home collateral mortgage as an alternative, that offers a lump sum for approximately 80% in your home security. This may be preferable in the event that financial rates of interest try high and you will you ought not risk replace your brand new mortgage with an effective large notice loan.

Similarly, you could use a home equity personal line of credit (HELOC) to get into your own residence’s security. Which have an effective HELOC, you can continually obtain from the personal line of credit until you reach the restriction.

An all-in-one Financial is an additional choice that gives you access to your own house’s collateral. So it mortgage functions as home financing, an effective HELOC, and a checking account. You’ll make most costs with the brand new loan’s dominant, but you can also use the guarantee and make a massive purchase, such as an advance payment.

The amount you could potentially use varies according to your individual facts as well as on your own lender’s rules. Generally speaking, loan providers create residents in order to acquire doing 80% of the home’s worth for an earnings-aside refinance. This means that you can discovered a profit fee from 80% of your own residence’s really worth without having the amount you will still owe on the their mortgage.

Oftentimes, borrowers must hold off at least six months immediately after to shop for a home to do a great re-finance. Although not, you need to ensure that you have adequate security about family while making an earnings-out refi you can.

Most refinances tend to be a term demanding you to stay in your house to have per year immediately after closure. Although not, you might buy an extra household otherwise vacation family before. Residents can usually be eligible for another type of home loan 6 months immediately after its refi is done.

Just how long does it shot have the funds from a beneficial cash-aside refi?

The new timeline getting a cash-out refi may vary commonly. They will take 45 in order to 60 days to shut for the a good refinance, and you may more than likely found their funds three months once closing.

Is it necessary to make use of the exact same bank with the new possessions?

You don’t have to make use of the same home loan company for the first household and your new possessions. Particular property owners will will always be and their completely new lender in order to improve the application form processes.

Homeowners can use a money-out refinance to buy next property should they possess adequate collateral within their number one quarters. Playing with a profit-away re-finance to shop for next property is a fantastic choice in the event that very first domestic has grown somewhat inside value of course, if the new industry criteria are ideal for and come up with a different pick. The biggest difficulties of many homeowners face when using dollars-away refinances to invest in next belongings is putting and timing the brand new processes so the funds appear in the event that down payment is necessary. To really make the feel as simple as possible, make sure you works close to a trusted home loan pro as you prepare for the refi.